In the latest of his regular updates Jisc's head of labour market intelligence, Charlie Ball, considers job vacancy trends, a report on balancing work and care responsibilities, and employment projections in the government's priority sectors

Data from the Office for National Statistics (ONS) showed that UK GDP rose by 0.3 per cent in the three months to June, and by 0.4 per cent in June, a modest but welcome rise.

There was a very modest month-on-month rise in vacancies in July 2025, following a slightly more substantial rise from the recent trough in May. However, overall, the estimated number of vacancies in the UK fell by 44,000 on the quarter, to 718,000 in May to July 2025.

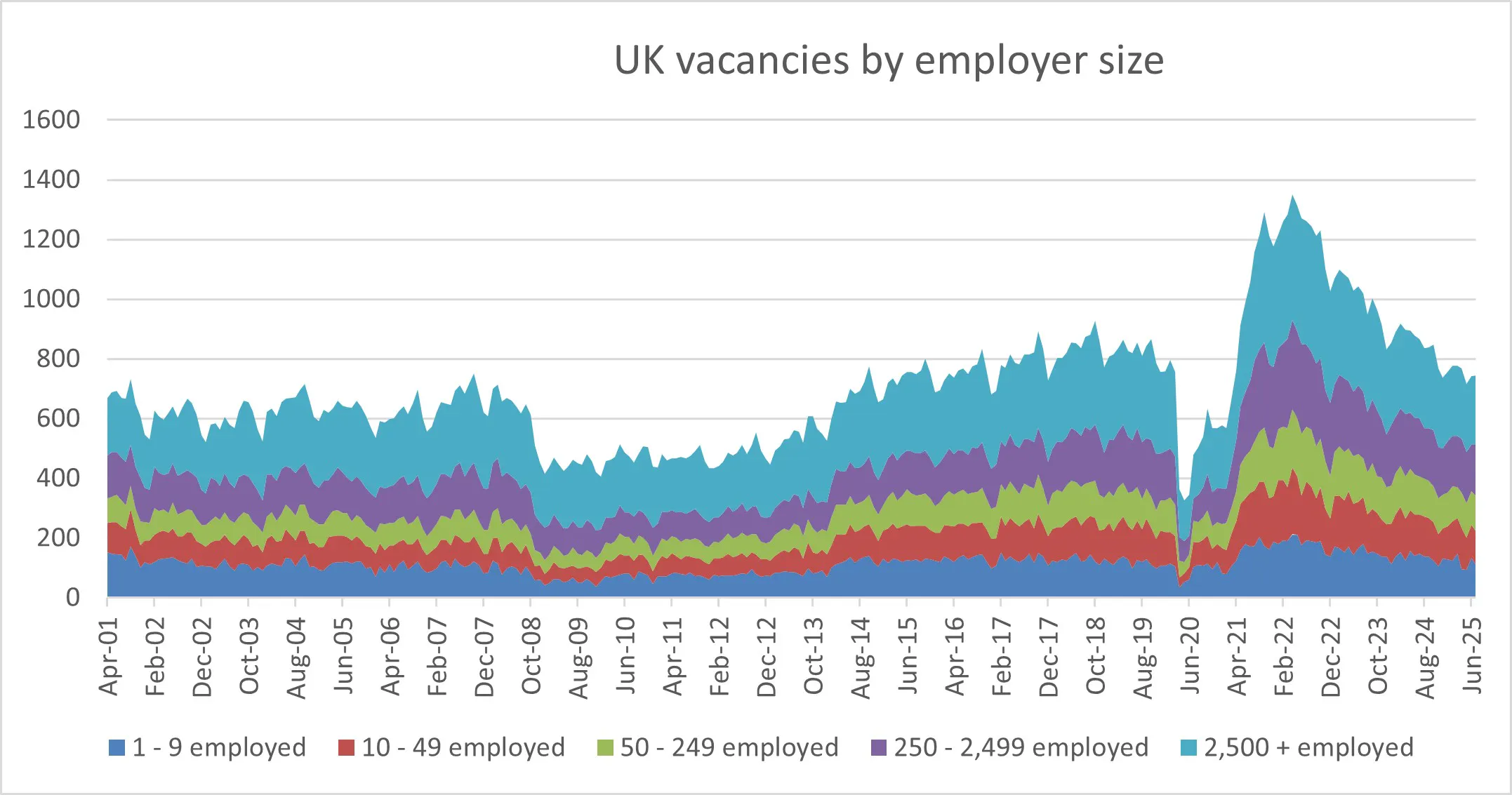

Plotting monthly data for all vacancies, it looks as if we're currently in a process of reverting to something like the long term trend, or perhaps slightly below that, but not in a recessionary state - yet. I've plotted the data by employer size back to 2001 below, so you can see where the peaks and troughs are. I have mentioned this in passing elsewhere but this really drives home quite how odd the post-COVID jobs market was - we haven't seen vacancy levels like the ones from mid 2021 to the end of 2023 for at least 20 years and probably ever, and until we collectively understand that then the current jobs market will seem weak in comparison to that period.

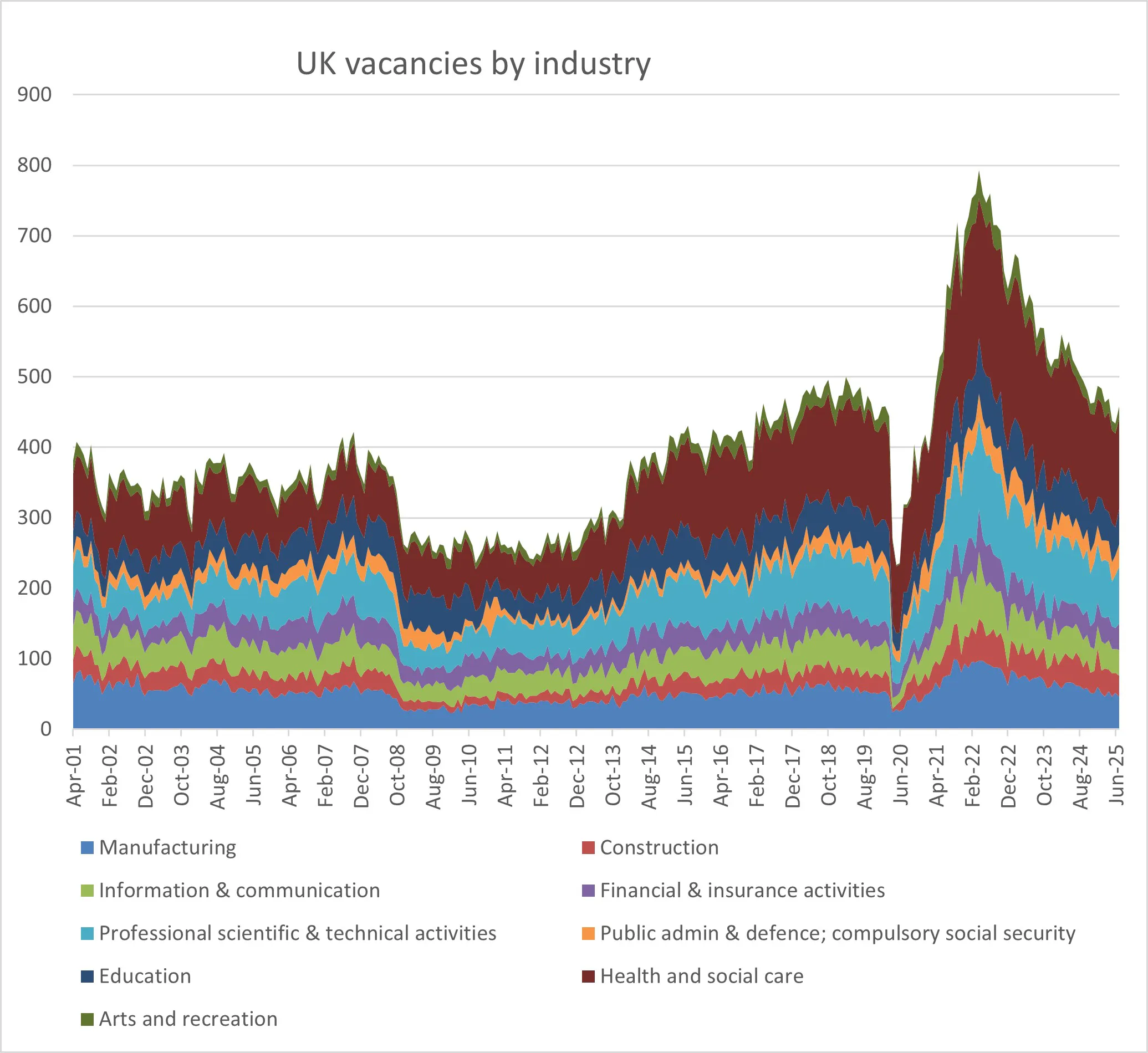

We can also look at vacancy patterns for major graduate-recruiting industries - this is a bit more complicated. I've left out some sectors like retail and services because although big recruiters, their roles usually (but not always) don't need degrees. This isn't a plot of graduate vacancies although it has some relationship to that measure.

One thing you notice is that retail is having a very tough time right now with vacancy-to-staff ratios particularly low. IT is an interesting case too, in principle with a high vacancy ratio (suggesting worker shortage), but lower than usual - so it might be more appropriate to say that the long-term shortage of IT staff that has become such a permanent feature of the UK labour market that people are just generally accustomed to it might actually be in the process of fading. It's far from clear that this really is due to AI as some proponents have been saying, but there seems to be something going on - that said, there are signs of recovery in the last three months in IT so even that might only be temporary.

The ONS does note that at present the fall in vacancies isn't necessarily being matched by a rise in redundancies, it seems to be more to do with firms not recruiting new workers or replacing workers who have left.

The total estimated number of vacancies is 77,000 (9.7%) below its January to March 2020 pre-pandemic level, although retail alone accounts for nearly half of that shortfall.

I like the Learning and Work Institute analysis of the headline figures, so take a look at their resources for more on those.

I've also received my own cut of the Graduate Outcomes data for 2022-23 leavers. I've not had much of a chance to look at it in detail, mostly just been doing some of the analysis for the next edition of What do graduates do? (which will be published here in November), but it's clear that whilst I still think the graduate jobs market isn't in a dire state at the moment, the negative changes last year were moderate but significant, and for some subjects, like IT, were a bit more substantial.

I can see the origins of some of the online narratives about a terrible market for graduates - it looks to have declined more steeply for IT graduates than for many others. And it also looks like the non-graduate labour market had a sticky time last year too, which means graduates who didn't secure a professional level job quickly - or lost one due to market changes - had fewer good alternative options and were more likely to end up in insecure, poorly paid work or outright unemployed. Again, it doesn't look like we're where we were in the last recession, and we're still coming down from an exceptional jobs market, but another set of changes of that magnitude and direction in the next dataset would be worrying.

The CIPD have released their new Labour Market Outlook, and it doesn't make great reading either. Net employment balance at +9, slightly up from last quarter. 57% of private employers have plans to recruit in the next three months, not a very strong figure.

In the public sector, the net employment balance stands at –6. Recruitment pressures have eased, but this reflects reduced hiring activity, particularly in the NHS, and could also be linked to the impact of July's changes to immigration rules and, in particularly the closure of the Social Care Worker route. The net employment balance in social care has dropped from +23 to –2.

The Recruitment & Employment Confederation's (REC) new Report on Jobs gives a similar story of continued job market decline. Demand for staff fell during July, and after a lull in the last couple of months, started to decline more steeply again. The availability of new workers rose.

Redundancies, as well as concerns over job security, were reported as key drivers of increased worker supply. In general, hiring activity seems to be falling due to weak confidence around the economic outlook and greater pressure on budgets due to recent increases in payroll costs.

London, and the retail sector, seem to be particularly affected but there seems to be little sign of recovery in the immediate future.

Balancing work and caring responsibilities

Back to the Learning and Work Institute, and they've released an interesting new report on balancing work and care responsibilities.

- More women than men report providing care. In 2021 to 2023, 61% of working-age carers were women. Women also provide more hours of care per week than men; 32% of female working-age carers provide 20 hours or more of care each week compared to 24% of male working-age carers.

- 20% of 60 to 64-year-olds report that they are carers compared to 7% of 16 to 29-year-olds. Carers aged 30-49 are more likely to be providing more than 20 hours of care per week.

- Care roles extend beyond an individual's working life; 25% of all carers are aged 65 or older.

- 9% of carers who spend 20 to 34 hours a week caring report being unable to work at all. This more than doubles to 19% for carers who spend 35 to 49 hours a week caring.

- Around seven in ten carers who spend fewer than 20 hours caring per week have a job, compared to fewer than half of carers who spend 20 hours or more caring per week.

- Carers are less likely to work in the construction, information and communication, and accommodation and food service industries than non-carers.

- Conversely, carers are more likely than non-carers to work in the public administration, education, and health and social work industries.

- More carers work in health and social care roles than any other industry; 22% of carers who are in work have a job in this industry, compared to 18% of non-carers.

- Industries where carers are overrepresented are dominated by public sector employers, which typically offer better job security and other terms and conditions of employment, such as carer's leave, than private sector employers.

- However, the experience of providing informal or unpaid care can sometimes influence carers to choose careers in paid caring roles - one survey of NHS staff found that one third of respondents also identify as unpaid carers outside their paid roles.

Meanwhile, the Department for Work and Pensions commissioned NatCen (the National Centre for Social Research) to conduct a review to better understand what works to support people from disadvantaged backgrounds to move towards and into employment. The report on care leavers has just been published. It's rare that I report findings of this kind but I think the topic is important to higher education, and the issue is that the review found that the evidence base was really rather weak. There's not a lot to summarise (quite a bit of 'there's not much evidence here' but it's worth reading the report simply to understand how many gaps there are.

Employment in priority sectors

And Skills England have just released employment projections for the government's priority sectors to 2030. Jobs in priority occupations are expected to expand significantly by 2030. That growth will outpace non-priority employment, and two thirds of the growth will be at Level 4 - higher education level - or higher.

Employment demand in priority occupations across the ten sectors is expected to increase by 0.9 million by 2030, from 5.9 million in 2025 to 6.7 million in 2030, an increase of 15%. This is 1.6 times faster than other employment in these sectors, which is expected to increase by 0.8 million, a 9% increase from 8.9 million in 2025. These estimates are subject to a high degree of uncertainty.

0.9 million doesn't sound like much, but that's in the next four-and-a-half years. Or, as two thirds are expected to come from HE, that's 600,000 graduates from the next four cohorts, or 150,000 graduates a year just into these sectors. As most of these prospective graduates are already in their courses, in practise, that means we have around a year to make up any shortfalls in course admissions.

There's data on individual occupations (we need 90,000 new care workers and 87,000 new coders, so maybe that IT downturn will be temporary after all), but one of the smaller numbers caught my eye - we're going to need 12,000 new civil engineers just into priority sectors (not including stuff like transport and infrastructure), which is a lot more than we're producing right now and anyone starting this year will be graduating in 2030, so that gives the UK around 2 months to convince rather a lot of people to train in civil engineering.

Written by

Was this page useful?

Thank you for your feedback